Copper's supply gap isn't a forecast anymore. It's showing up in real numbers, right now.

For two decades, the global copper market could rely on a simple playbook: Chile and Peru produced half the world's mine supply, China smelted it, and demand grew at a steady 2-3% clip. That playbook broke sometime around 2023. Green energy buildouts, EV production ramps, and grid modernization campaigns collided with a mining sector that hadn't invested in new capacity since the early 2010s. And the deficit that analysts warned about for years? It's here.

This isn't a story about one quarter's inventory drawdown. It's about a structural mismatch between what the world needs and what the ground can deliver over the next decade.

Mine Supply Peaked While Nobody Was Watching

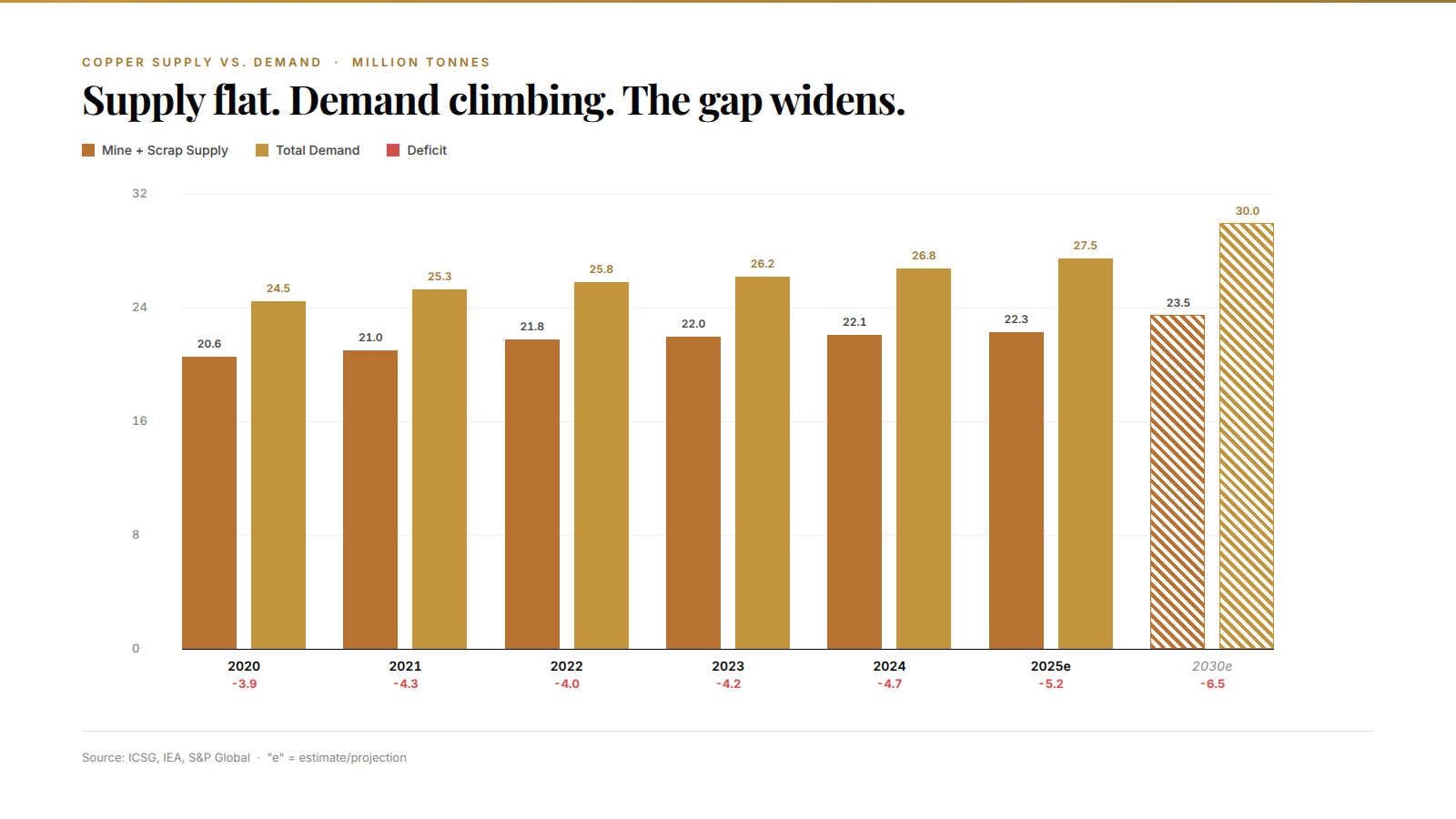

Here's the uncomfortable truth: global copper mine output has barely grown since 2018. Total production sits around 22 million tonnes per year, and that number hasn't moved much. Chile's state-owned Codelco, the world's largest producer, has watched its output slide from over 1.8 million tonnes a decade ago to roughly 1.4 million tonnes. Ore grades at legacy deposits in Chile and Peru are declining. And declining fast.

Escondida, the world's biggest copper mine, now processes ore that's about 30% lower grade than what it ran a decade ago. That means more rock moved, more water used, more energy burned, all for less copper per tonne of dirt. The same pattern plays out at Grasberg, Cerro Verde, and Antamina.

But aren't there new mines coming online? Sure. A handful. Kamoa-Kakula in the DRC has been a genuine bright spot, ramping toward 600,000 tonnes. QB2 in Chile finally started producing after years of delays and cost blowouts. But these additions don't offset the decline at legacy operations, let alone cover demand growth. S&P Global estimates the industry needs to bring roughly 8 million tonnes of new annual capacity online by 2035. That's the equivalent of building eight Escondidas in nine years. Nobody thinks that's happening.

Green Demand Is the Accelerant, Not the Whole Story

The energy transition gets all the headlines. And it's real. An electric vehicle uses roughly 80 kilograms of copper, compared to about 23 kilograms in a conventional car. A single offshore wind turbine can require 15 tonnes. Solar installations eat about 5.5 tonnes per megawatt.

But here's what most green-transition copper stories miss: the grid itself is the biggest demand driver. For every megawatt of renewable capacity installed, you need transmission lines, transformers, substations, and distribution upgrades. Grid copper demand is growing at roughly double the rate of EV copper demand. The IEA's latest numbers suggest grid-related copper consumption could double by 2035 from current levels, adding something like 5-6 million tonnes of annual demand on top of what we already consume.

China alone installed over 900 gigawatts of solar and wind capacity in 2024 and 2025 combined. Each gigawatt needs grid infrastructure to connect it. That's not a one-time purchase. Every year the renewables fleet grows, the grid copper bill grows with it.

And traditional demand hasn't disappeared. Construction, industrial machinery, consumer electronics. These sectors still account for over 60% of global copper consumption. They're not shrinking. My guess is that total demand hits 30 million tonnes by 2030, maybe sooner if India's grid buildout accelerates the way Delhi keeps promising.

The 15-Year Problem Nobody Wants to Talk About

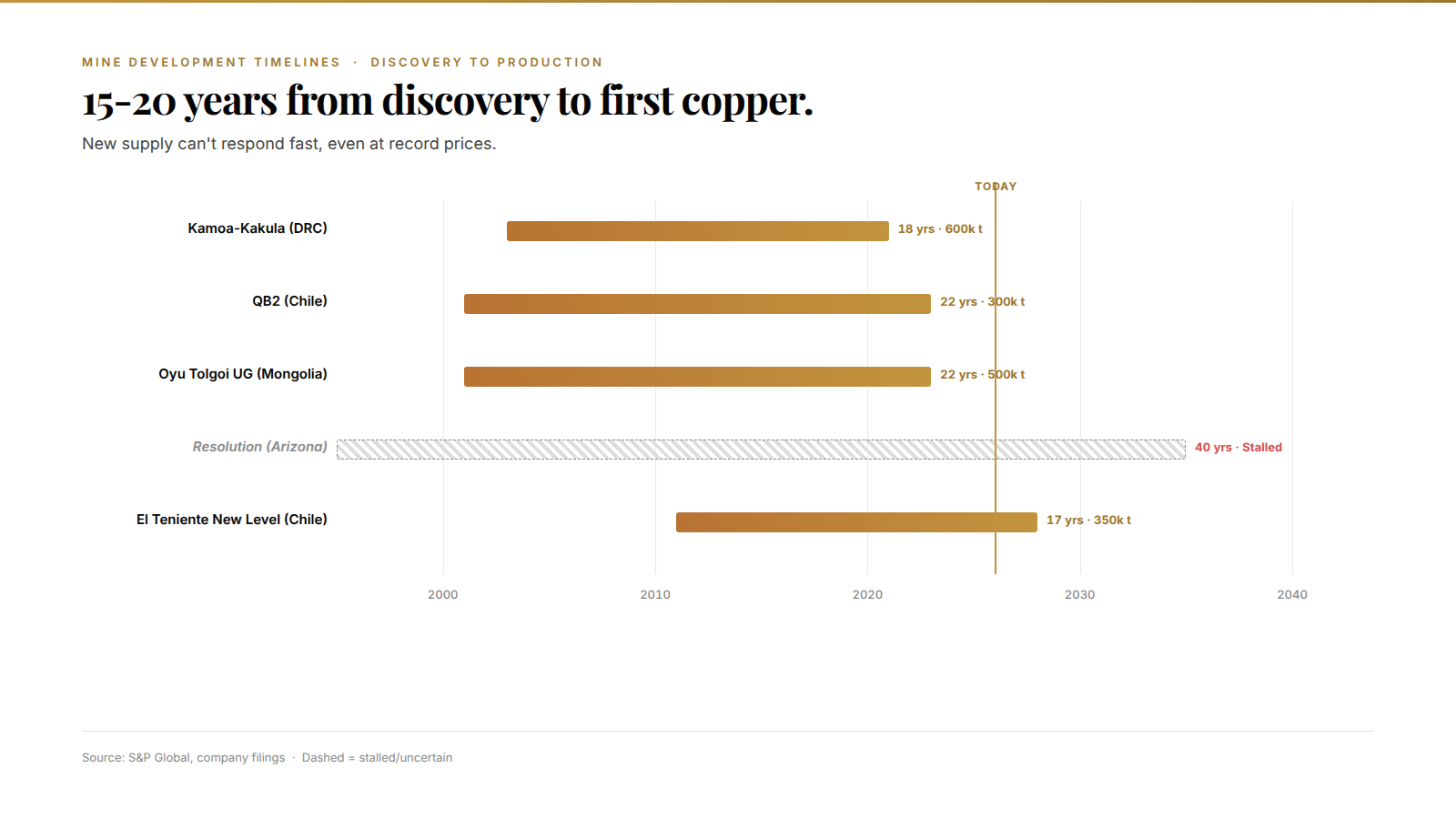

New copper mines don't appear overnight. The average timeline from discovery to first production is 15 to 20 years. That's not a conservative estimate. That's what the data actually shows.

Consider Ivanhoe's Kamoa-Kakula. Robert Friedland identified the deposit in 2003. First copper came in 2021. Eighteen years. And Kamoa had unusual advantages: a supportive host government, a billionaire backer with deep pockets, and genuinely world-class ore grades.

Most new discoveries don't have those luxuries. Permitting timelines in Chile have stretched to 8-10 years for environmental approvals alone. Community opposition, water rights disputes, and regulatory uncertainty have killed or stalled projects across Latin America and Southeast Asia. Resolution Copper in Arizona, one of the largest undeveloped deposits in the world, has been in permitting limbo for over a decade with no clear path forward.

So even if copper prices rip to $6 or $7 a pound (and some analysts see that coming), the supply response can't happen fast. You can't mine what you haven't permitted, built, and staffed. The capital cycle in mining is brutally slow, and the industry spent 2013 to 2020 cutting exploration budgets, closing offices, and buying back stock instead of drilling.

The numbers are stark. Global copper exploration spending peaked around $10 billion in 2012. By 2016 it had dropped below $4 billion. It's recovered since then, but exploration dollars today go less far because the easy deposits have been found. What's left tends to be deeper, lower grade, in more remote locations, or in jurisdictions with higher political risk. The discovery pipeline that would normally feed production 15 years from now is running thin.

China's Import Machine Isn't Slowing Down

One of the clearest signals that the deficit is real: China's copper concentrate imports hit all-time highs recently, with full-year volumes running up 28% to roughly 17 million tonnes. And that's just concentrate. Refined copper imports stay elevated too, with bonded warehouse inventories sitting well below historical averages.

China's smelting capacity has expanded faster than its access to raw material. Treatment and refining charges (TC/RCs), the fees smelters charge to process concentrate, have collapsed to near-zero and even gone negative. That's a smelter-capacity-overshoot problem layered on top of a mine-supply problem. Smelters are bidding aggressively for scarce feed, eating margins to keep furnaces running.

Wait, actually. That dynamic is worth sitting with for a second. The smelting industry built capacity expecting mine supply growth that didn't come. Now they can't get enough raw material. That's not a demand problem broadcasting through the chain. That's a supply problem.

This isn't sustainable. Some marginal Chinese smelters will get squeezed out. But the ones that survive will keep pulling concentrate from global markets, tightening the physical balance for everyone else.

Recycling Won't Save the Math

Scrap copper (secondary supply) covers about 30% of global refined production. That's meaningful. And it's growing. Urban mining, electronic waste recovery, and better collection infrastructure in Europe and North America are incrementally positive.

But recycling has physical limits. You can't recycle copper that's still embedded in buildings, cables, and infrastructure with decades of remaining useful life. The average age of copper in use globally is something like 25 to 35 years. So the copper installed during the last building boom isn't available for recycling yet.

And even optimistic scenarios from the International Copper Study Group project scrap supply growing at 2-3% a year. That doesn't close a gap that's widening at 4-5% on the demand side. Wait, actually, the gap math is worse than that. If demand grows 3-4% and primary supply grows under 1%, scrap at 2-3% growth barely keeps the shortfall from accelerating.

Recycling is part of the answer. It's not the answer.

What Price Does the Market Need?

Here's where it gets interesting for traders. Copper has been the best-performing base metal over the last two years, and it probably hasn't priced in the full extent of the structural deficit yet.

The incentive price to bring new greenfield capacity online is somewhere north of $4.50 a pound, probably closer to $5.00 when you factor in today's capital costs, ESG compliance requirements, and longer permitting timelines. Some industry consultants put the long-run incentive price at $5.50 or higher.

I don't know exactly where the clearing price lands. Nobody does. But the directional bet is straightforward: if demand grows at anything close to what the IEA, ICSG, and S&P Global project, and supply can't respond for 10 to 15 years because of the development timeline, the price has to go high enough to ration demand. That means $5, $6, maybe higher in real terms over the next decade.

The counterargument is demand destruction. At high enough prices, substitution kicks in. Aluminum replaces copper in some wiring applications. Fiber optics displace copper telecom cable. But these substitutions are slow, partial, and don't apply to the highest-growth segments (EVs, grid, renewables). You can't build a transformer with aluminum windings and get the same performance. And data centers, the newest copper demand story, aren't substituting away from it either. Every AI server rack needs copper for power delivery and cooling. That's incremental demand nobody was modeling three years ago.

There's also the geopolitical angle. Resource nationalism is ticking up in copper-producing countries. Chile's royalty reform, Peru's ongoing social license battles, Indonesia's export restrictions on raw materials. These don't reduce long-term demand. They constrain supply further and push up the cost curve for producers trying to get metal out of the ground.

The Structural Trade Isn't Crowded Yet

Big macro funds have copper exposure. That's not new. But real positioning for a multi-year supply deficit is still early innings. Mining equities trade at historically low multiples relative to the copper price. Exploration-stage companies with permitted deposits are being valued as if the deficit doesn't exist.

The opportunity here isn't just the commodity. It's the entire supply chain: miners with long-life reserves, recyclers scaling urban mining operations, and equipment manufacturers building processing capacity the industry desperately needs.

At Kunkel Capital, this is exactly the kind of structural dislocation we track across commodities, macro, and equity markets. The copper deficit is one data point in a broader theme: critical materials bottlenecks that will define capital allocation for the rest of this decade.

Last updated: April 2026